Insurance is when you pay money regularly to an insurance company to protect yourself or your business from problems you don’t expect. This money you pay is called a premium. If something bad happens—like an accident, illness, or damage—the insurance company helps pay for those costs according to what your policy says. Your policy is a paper that explains what is covered and how to claim money. The company collects premiums from many people and puts it together in a big pool of money. When someone faces a loss, the company uses this pool to help them. This way, everyone shares the risk, so no one loses a lot of money alone. Insurance keeps you safe from big money problems and gives you peace of mind.

Insurance

Types of Insurance

Category: Life Insurance

Term Life Insurance

Term insurance is a type of life insurance that provides financial security for a specified period, or the "term," typically ranging from five to forty years. The policyholder pays regular premiums under this contract, and the insurer pays a death benefit to the designated beneficiaries if the policyholder passes away during the term. There is no payout if the policyholder lives out the term, unless a Return of Premium (ROP) rider is bought. In the event of an unexpected death, term insurance is a good option to protect one's family's financial future because of its simplicity, cost, and high coverage amounts. Unlike permanent life insurance, it only focuses on risk protection and does not increase cash value. The protection provided by the base policy can be improved with additional riders and adjustable payout choices. Because of this, term insurance is a well-liked option for protecting families and replacing income during stressful times like raising kids or mortgage repayment.

Whole Life Insurance

Whole life insurance is a kind of permanent life insurance that, provided premiums are paid regularly, covers the policyholder for the duration of their life. Whole life insurance ensures a death payment to the beneficiaries whenever the insured person dies, usually up to age 99 or 100, compared to term insurance, which protects for only a limited period of time. Moreover, whole life insurance builds up a cash value component over time that is accessible to the policyholder through loans or withdrawals made during their lifetime and increases tax-deferred. Predictability and financial security are provided by premiums, which are typically fixed and do not rise with age. Because it offers lifetime protection with both insurance coverage and a savings component, this policy is frequently used for long-term financial planning, estate planning, and wealth transfer. Additionally, certain policies might generate dividends that can be applied to higher coverage or lower rates. All things considered, whole life insurance is a complete tool for legacy planning and lifetime financial stability since it combines a death benefit with a savings element.

Endowment Policy

An endowment policy is a type of life insurance plan that helps you save money while providing financial protection. You pay regular premiums for a fixed time, usually between 10 and 30 years. If you pass away during this time, your family gets a guaranteed amount of money, called the sum assured, which gives them financial support. If you live through the policy term, you receive a lump sum payment when the plan ends. This payout usually includes the sum assured plus some extra bonuses or returns. Endowment policies are good for people saving for big goals like education, retirement, or paying off a loan. The premiums you pay often help you save on taxes, and the money you get later may also be tax-free. So, this type of policy helps you both protect your family and build savings in a steady, disciplined way. It also offers flexible premium payment options and the potential for guaranteed returns with low risk.

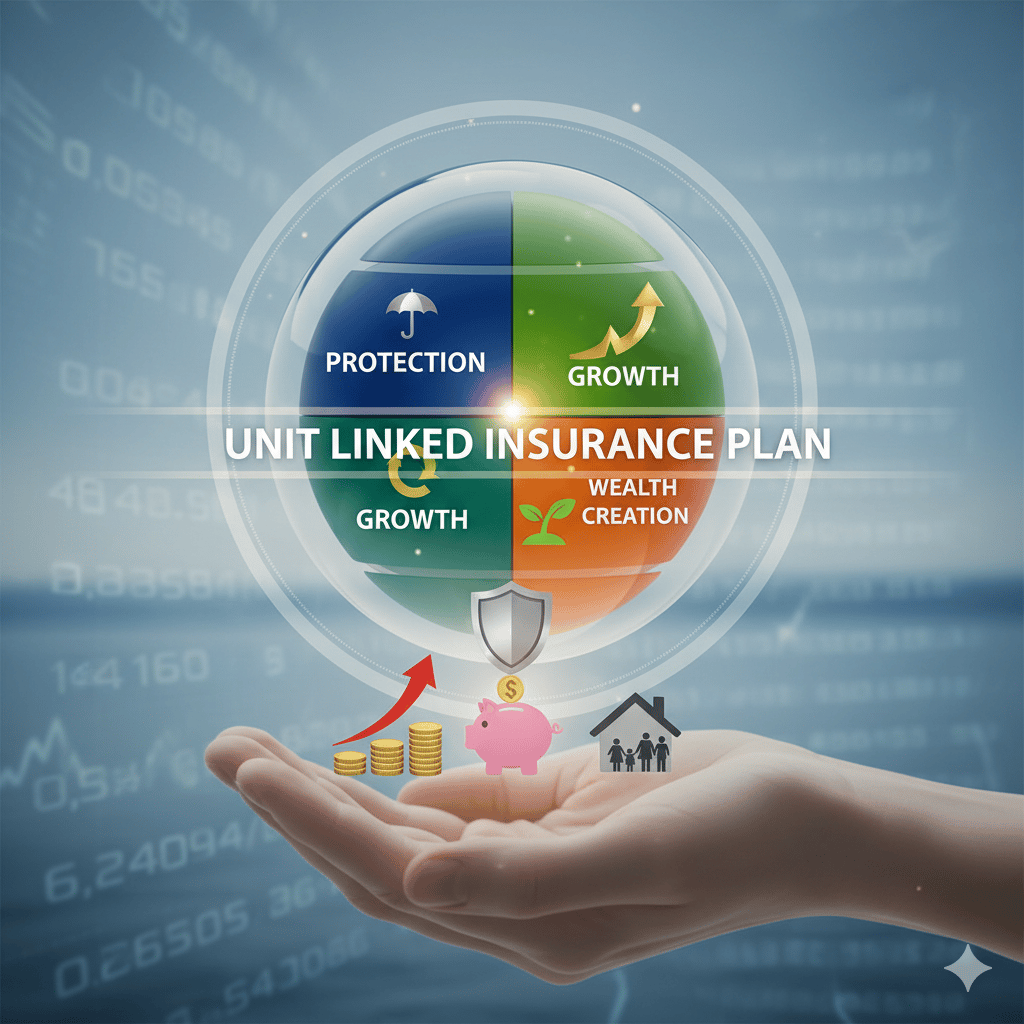

Unit Linked Insurance Plans (ULIPs)

A financial plan called a Unit Linked Insurance Plan (ULIP) combines the advantages of investment with life insurance. A percentage of the premiums you pay for a ULIP is used to cover life insurance, and the rest is invested in market-linked funds like debt, equity, or hybrid funds, depending on your investing objectives and risk tolerance. This double advantage allows policyholders to increase their wealth through investments and safeguard their family's financial future through insurance cover. With features like fund switching—which lets you transfer investments between funds without incurring taxes—partial withdrawals following a lock-in period, and the ability to top up your investments, ULIPs provide flexibility. Strong financial protection is ensured by the nominee receiving the higher of the sum promised or the fund value in the case of the policyholder's death. Additionally, ULIPs offer tax advantages on premiums paid. These plans cater to varying levels of risk and investment horizons and are managed by certified fund managers to get maximum returns.

Child Insurance Plans

A child insurance plan is a type of specialist life insurance policy that combines investment and insurance coverage to protect a child's financial future. In the tragic event of the insured parent's death, it mainly offers financial support to the child, guaranteeing that the child's education and necessities are met without causing financial hardship. These programs provide a lump sum payout or recurring payments that coincide with important life events for the child, such as marriage, college, or other big costs. Furthermore, child insurance policies provide tax advantages under Indian law and assist parents in methodically investing for their child's future requirements by accruing a maturity amount that increases over time. Additionally, future premiums are usually waived if the parent dies during the policy term, but the plan still offers coverage until maturity, guaranteeing continued financial stability. Additionally, these plans occasionally permit loans or partial withdrawals to supply cash in times of need. In general, the goal of child insurance plans is to provide parents peace of mind by protecting their children's financial security by combining safety with frugal saving.

Retirement or Pension Plans

Plans for retirement or a pension are financial agreements created to give people a consistent income once they leave the workforce, guaranteeing their financial stability in their later years. These programs involve building up assets or savings throughout one's working years, which are subsequently transformed into pensions or annuities—regular payments—after retirement. Pension plans come in a variety of forms, such as immediate annuity plans, which pay out immediately following a lump sum investment, and delayed annuity plans, which pay out after a waiting time. In India, government-sponsored programs like the Employee Provident Fund (EPF) and National Pension Scheme (NPS) are well-liked because they provide a range of investment alternatives and tax advantages. Life insurance may also be included in pension plans to ensure dependents' financial stability. After retirement, people can comfortably pay their expenses and continue their lifestyle thanks to the corpus created by these programs.

Category: General Insurance

Health Insurance

Health insurance is a kind of insurance that covers medical costs caused by disease, accidents, or other health-related problems. It is a financial security plan in which a policyholder pays a regular payment to an insurance company, which promises to pay for certain medical expenses specified in the policy. Health insurance's primary goal is to lessen the financial strain caused by growing healthcare expenses so that people can promptly receive medical care without worrying about money. Expenses for hospitalisations, operations, prescription drugs, preventative care, and even serious illnesses are usually covered. Additional perks, including cashless medical procedures, network hospital access, and tax savings under applicable tax rules, are also provided by many health insurance policies.

Motor Insurance

All forms of motor vehicles, including cars, trucks, buses, two-wheelers, and commercial vehicles, are financially protected by motor insurance, which is a mandatory insurance type. It was created to cover loss or damage to the insured vehicle brought on by theft, fire, natural disasters, or accidents. Furthermore, in an accident involving the insured vehicle, automobile insurance shields the policyholder from legal obligations resulting from harm or property damage to third persons. There are primarily two forms of automobile insurance coverage: comprehensive insurance, which offers greater coverage, including damages to the insured vehicle and personal accident cover for the driver, and third-party insurance, which is legally required and only covers third-party liabilities. By reducing the costs of auto repairs, medical bills, and legal claims, auto insurance offers both the car owner and other parties involved in auto accidents financial stability and peace of mind.

Home insurance, also called homeowner's insurance, helps protect your house and everything inside it from damage or loss caused by unexpected events like fire, theft, storms, floods, or earthquakes. It also provides coverage if someone gets hurt on your property or if you accidentally damage someone else's property. When you buy home insurance, you pay a regular amount called a premium. In return, the insurance company helps cover the cost to repair or rebuild your home, replace your belongings, and handle any liability claims. This insurance gives you peace of mind by reducing the financial burden caused by accidents or disasters, making sure your home and possessions are safe and secure.

Home Insurance

Travel Insurance

Travel insurance is a kind of insurance designed to protect against the different hazards and monetary losses that tourists, whether domestic or foreign, may experience when travelling. Medical emergencies that may not be fully covered by standard health insurance are usually covered, including accident and illness care overseas. Travel insurance also protects against lost or delayed luggage, lost passports, aircraft delays, trip cancellations, and other travel-related inconveniences. Personal accidents, emergency evacuation, repatriation of remains, and other unanticipated events that may arise during travel may also be covered. By providing financial protection against unexpected expenditures and assisting in the handling of crises while away from home, this insurance provides travellers with peace of mind. Policies can be customized with extra advantages based on certain travel requirements, such as adventure sports or pre-existing medical concerns. Typically, the coverage lasts from the day of departure until the return.

Fire Insurance

Fire insurance is a form of property insurance that provides financial protection against damage or loss caused by fire incidents. It covers the cost of repairing, rebuilding, or replacing property damaged due to fire, including buildings, equipment, inventory, and personal belongings. Policyholders pay regular premiums to maintain this coverage. In the event of a fire, the insured reports the incident to the insurance company, which evaluates the claim and provides compensation based on the policy terms. Fire insurance often extends to related perils such as lightning, explosions, and certain natural disasters. This insurance is essential for both individuals and businesses to mitigate financial risks and ensure continuity after fire-related losses, offering peace of mind and financial security in unforeseen circumstances.

Marine Insurance

Insurance that covers ships, cargo, and items being carried from one location to another, particularly across the sea, is known as marine insurance. Any loss or damage that may occur during the trip, such as storms, accidents, theft, or piracy, is covered. Marine insurance covers goods transported by air, road, or rail as part of the shipping process, even though it was initially created for maritime transportation. If something goes wrong with the products during transit, the insurance assists buyers, sellers, and shipping businesses in avoiding significant financial damages. The insurance company and the owner of the cargo or ship enter into a contract whereby the insurance company promises to pay for specific losses in exchange for a premium. For international trade to remain secure and function properly, marine insurance is crucial.

Crop Insurance

Crop insurance is a specific type of agricultural insurance designed to protect farmers from financial losses resulting from declines in revenue or production due to adverse farming conditions. It helps farmers pay for inputs like seeds, fertiliser, labour, and equipment by offering compensation when crop yields are lower than anticipated or when prices decline. A defined group of crops within a region is covered by the majority of crop-insurance plans, which are area- or yield-based and frequently include government assistance or subsidies to make coverage reasonable for farmers. In general, farmers usually pay a premium, and the policy's conditions, coverage limitations, deductibles, and reporting requirements specify how much of the loss is covered by the insurer through claims. By lowering the financial risk connected to weather extremes, pests, illnesses, and other natural uncertainties, this safety net promotes investment in crops and farming methods.

Liability Insurance

Businesses and individuals can obtain financial protection from liability insurance against lawsuits claiming that third parties were harmed or that their property was damaged. If the insured is found legally responsible for unintentional harm or damages, it covers legal fees as well as any compensation that may be required. Because it protects other parties rather than the insured, this insurance is frequently referred to as third-party insurance. Intentional harm, criminal activity, and contractual liabilities are usually not covered. To protect against the potentially high expenses of lawsuits or claims originating from accidents, negligence, or product flaws, liability insurance is crucial for business owners, professionals such as doctors and lawyers, and car owners. Liability insurance helps policyholders preserve their financial stability and safeguard their assets in the event of legal claims by paying for settlements and legal costs.

Ways to find good insurance

Understand Your Insurance Needs

You must specify your goal before purchasing any insurance. Your age, life stage, income, dependents, and ambitions are just a few of the financial and personal variables that affect your insurance needs.

A term life policy is the finest option for financial protection because it provides substantial coverage at a low cost.

Invest in comprehensive health insurance to protect against catastrophic illnesses, hospitalization, and pre- and post-treatment care.

ULIPs (Unit Linked Insurance Plans) or endowment plans that combine insurance and savings are good options for investment-cum-protection.

Consider purchasing home, auto, or travel insurance to protect your assets.

Determine Adequate Coverage

In the event of your absence or a medical emergency, the coverage amount—also referred to as the sum insured or sum assured—should be sufficient to meet your possible liabilities and preserve your family's standard of living.

To cover family expenses, debts, and long-term obligations like retirement planning or your children's schooling, choose life insurance that is at least 10 to 15 times your yearly salary.

Make sure your health insurance coverage is sufficient to pay for your family's hospital stays and medical expenses. Given escalating medical inflation, your health coverage should roughly equal between 50% and 100% of your yearly income.

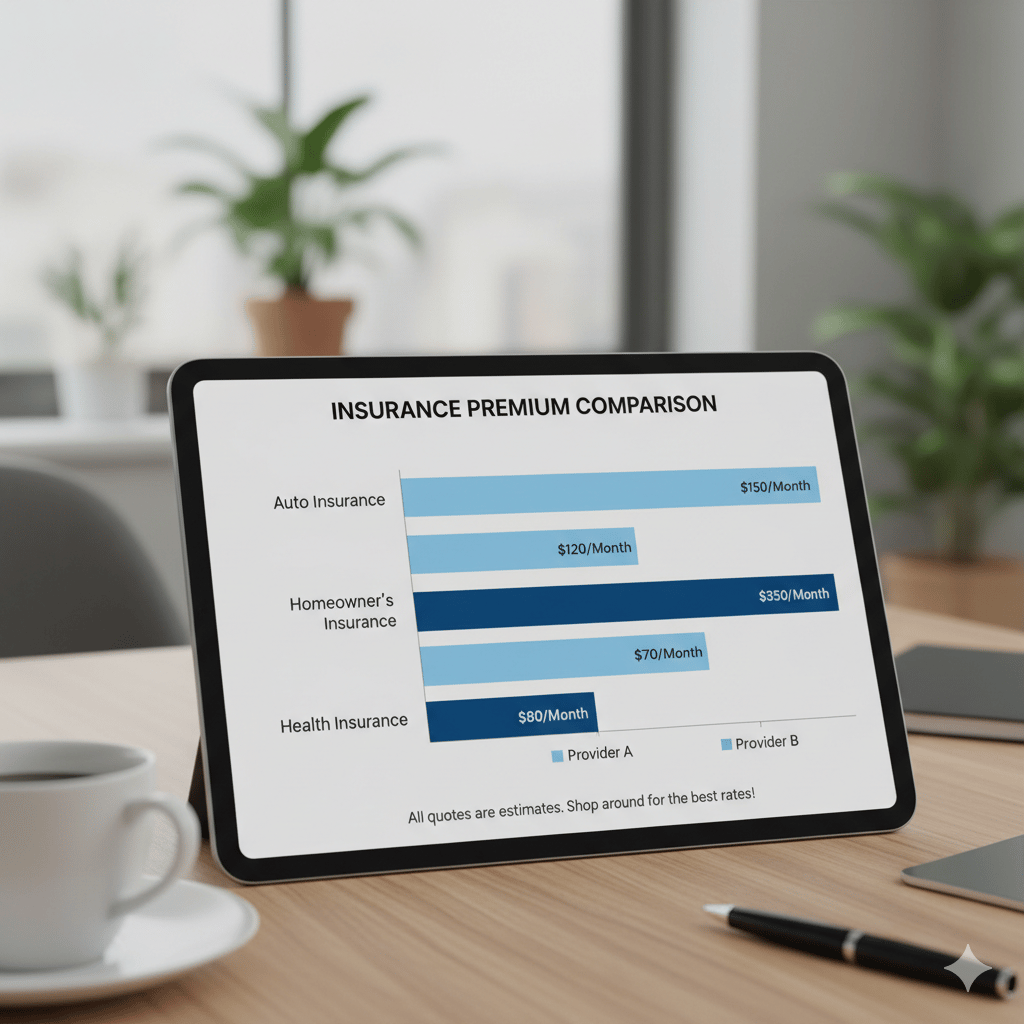

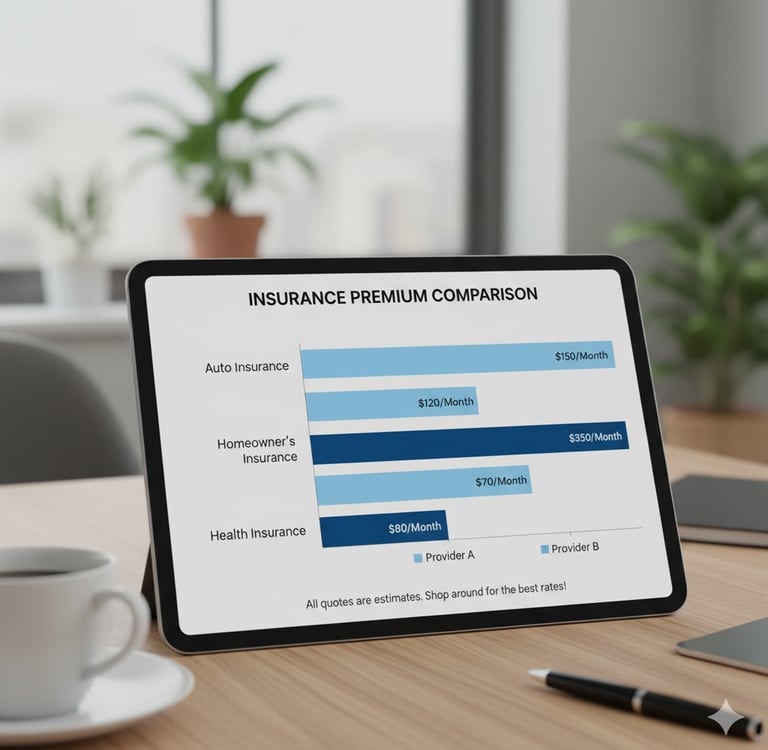

Compare Plans & Premiums

Pricing, terms, and inclusions vary among insurance companies. Utilize internet comparison resources to examine:

Make sure the premium is affordable for the duration of the coverage.

Riders and benefits, like critical illness, unintentional death, or long-term disability.

Flexibility: whether the insurer permits gradual policy term modifications, coverage upgrades, or partial withdrawals.

Note: Don't choose a policy just because it's the least expensive. Always evaluate the features and coverage you get in relation to the premium you pay.

Evaluate The Insurer's Reputation

The reliability of the insurance provider is crucial. Analyse key indicators like:

Claim Settlement Ratio (CSR): Indicates the proportion of claims the insurer settles annually. Choose insurers with CSR above 95% over multiple consecutive years.

Customer Service Feedback: Review claim timelines, customer experiences, and ease of communication.

IRDAI Data: Visit the Insurance Regulatory and Development Authority of India (IRDAI) website to verify company performance and reliability.

Read Policy Carefully

Read the policy conditions carefully before completing the transaction to fully understand co-payment clauses, deductibles, waiting periods, and exclusions. Many claims are denied because these details are not disclosed or are misunderstood. For openness:

Always disclose any past medical history as well as lifestyle choices, including drinking, smoking, or having chronic illnesses.

Recognise the paperwork required for a seamless settlement and the claim procedure.

Determine the conditions for renewal and lock-in periods.

Buy Early and Review Regularly

If you buy insurance when you're young, your rates will stay low, and over time, you'll get more security benefits. Review and modify your insurance coverage when your life changes, such as when you get married, have kids, or earn more money, to keep it in line with your evolving financial obligations.

Additional Tips for Smart Insurance Planning

Examine pre-existing condition coverage, cashless claim options, and network hospitals when selecting health insurance.

For better protection, consider adding riders to your life insurance, such as critical illness, accidental death, or a premium waiver.

Keep track of all policy documentation, premium receipts, and claim contact information.

Consult a certified insurance expert or financial planner if you are unclear about the policy to choose.

Follow us on

Smart Money Management is a finance platform dedicated to helping people make smarter decisions about earning, investing, and managing money.

Quick Links

Contact Us

smm@smartmoneymanagement.site

© 2026 Smart Money Management. All Rights Reserved