New NPS Withdrawal Rules

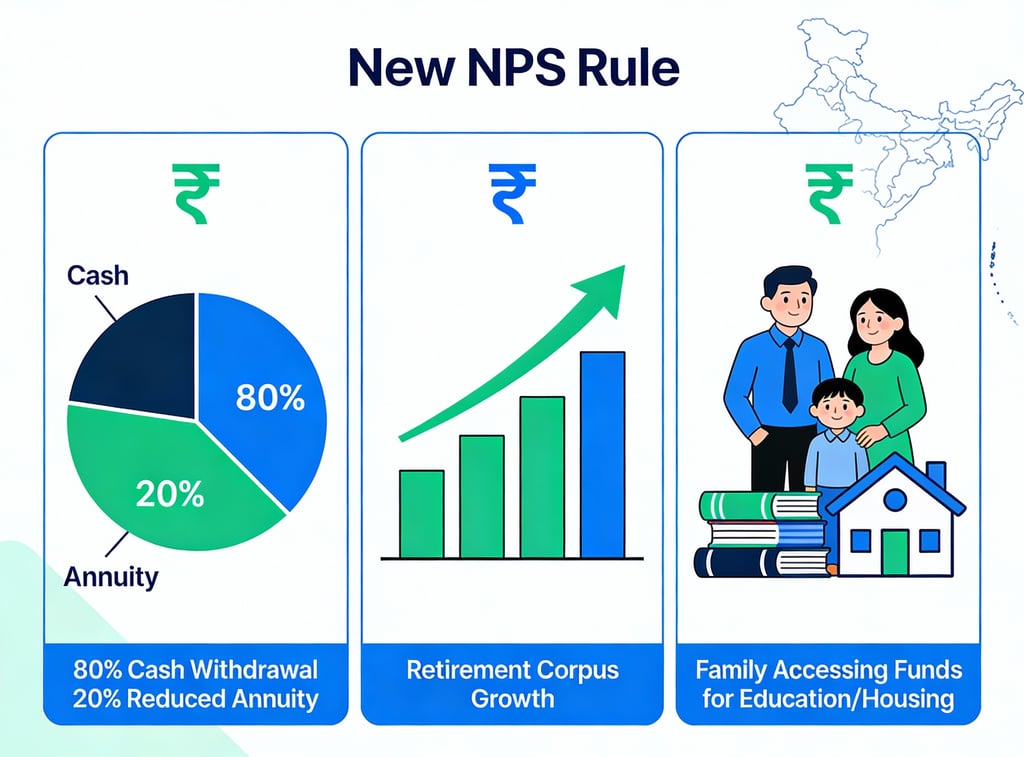

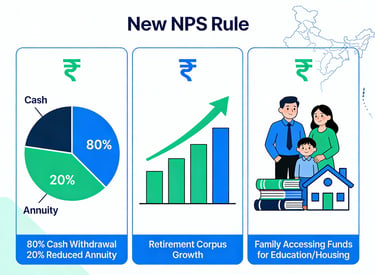

PFRDA has updated NPS rules to make withdrawals easier. Subscribers can now take up to 80% of their corpus as cash at retirement, with only 20% for annuity, and 100% if under ₹8 lakh.

MARKET NEWS

12/19/20252 min read

Through the PFRDA (Exits and Withdrawals under the NPS) Amendment Regulations, 2025, which were announced on December 12 and came into effect immediately, the PFRDA has implemented significant changes to the National Pension System (NPS) exit and withdrawal regulations. These modifications strike a balance between annuity obligations for long-term security and increased flexibility for both government and non-government subscribers, making retirement resources more accessible.

Key Withdrawal Changes

With only 20% required for annuity purchases—down from the previous 40%—non-government subscribers can now withdraw up to 80% of their corpus as a lump amount at exit (age 60+), greatly increasing liquidity.

If the total corpus is ₹8 lakh or less, a full 100% lump-sum withdrawal is permitted; if it is between ₹8 and ₹12 lakh, up to 80% can be withdrawn in one lump payment, with the remaining amount coming from annuities or recurring withdrawals.

The number of partial withdrawals made during a subscription increased from three to four times, with a four-year (formerly five-year) break, to accommodate additional uses such as housing, marriage, or study.

Up to three partial withdrawals with three-year intervals are permitted after superannuation (age 60+), and if the corpus remains invested, there is no annuity requirement.

Extended Exit Age and Deferrals

For people who do not require immediate income, subscribers can postpone exiting or purchasing an annuity until they are 85 years old.

Central and state government workers retain a 40% annuity and a 60% lump sum, but they have aligned deferral options up to 85.

New clauses about specific-purpose NPS programs, absent subscribers deemed deceased (family access), and exit on renunciation of citizenship.

Other Notable Updates

Applies consistently to all NPS models, including corporate, all-citizen, government, and NPS-Lite/Swavalamban.

Unlike unit redemptions, Systematic Lump Sum Withdrawal (SLW) offers more transparent post-exit choices.

Financial aid against the NPS corpus is now available from approved lenders, and there are no vesting requirements for anyone joining after age 60.

Implications for Subscribers

By emphasizing lump-sum access and flexibility, these revisions make NPS more appealing and may attract more retail investors in the face of growing AUM. However, given India's longevity trends, experts suggest striking a balance between lump amounts and annuities for steady retirement income. Changes are applied prospectively to current subscribers; see POPs or CRA for specific effects.

Follow us on

Smart Money Management is a finance platform dedicated to helping people make smarter decisions about earning, investing, and managing money.

Quick Links

Contact Us

smm@smartmoneymanagement.site

© 2026 Smart Money Management. All Rights Reserved